Insurance Insights : From Edward Lloyd’s Coffee House to Europe: A Journey Into the Heart of a Unique Market

article 10 minutes 02.12.2025

Insurance Insights : From Edward Lloyd’s Coffee House to Europe: A Journey Into the Heart of a Unique Market

« Lloyd’s does not only insure ships or buildings. It insures trust, reputation, and the courage to imagine the unimaginable.»

A statement attributed to a former Lloyd’s Chairman in the 1990s.

« How amusing! There truly is no such thing as coincidence, and yet…»

Martial de Calbiac

For someone like me, who has devoted nearly 50 years of his life to insurance (and reinsurance!), it is quite striking that, in the very same week, I came across this archive while sorting through my papers, and I was approached by the ACA to write an article about Lloyd’s.

The loop is now fully closed: after almost starting my career by working with Lloyd’s locally in London when I was at Gras Savoye and Willis Faber, I am ending it as the legal representative of Lloyd’s Europe in Luxembourg, after having practised numerous insurance and reinsurance professions between 1976 and 2025 (in Paris, London and Luxembourg).

One cannot talk about Lloyd’s without talking about its history. Certainly, Lloyd’s is a highly modern entity, but it is built on a very long-standing tradition.

A singular and centuries-old insurance market, Lloyd’s (often referred to as “Lloyd’s of London”) is not an insurance company in the usual sense: it is a market where capital (grouped into syndicates) takes on risks, brokers bring in business, and the Society of Lloyd’s organises, regulates and provides central services.

This article traces its origins, revisits the severe crisis of the 1980s–1990s, explains the structural transformation that enabled the massive entry of so-called corporate capital, and describes the market’s current operation. It also presents some recent figures, the creation of Lloyd’s Insurance Company in Brussels, and the related challenges.

Lloyd’s has its roots in a coffee house founded by Edward Lloyd in London at the end of the 17th century, where sailors, shipowners and brokers exchanged maritime information and placed risks. From this place emerged, over the decades, the practice of a specialised market and various derivative institutions (ship lists, classification, etc.). Through parliamentary acts (notably the Lloyd’s Act of 1871 and later consolidations), the structure gradually became more formalised: Lloyd’s became a legal entity endowed with its own framework, while remaining a place where underwriters and risk-takers met and conducted business.

In the 1980s and early 1990s, Lloyd’s suffered massive losses, particularly linked to so-called long-tail claims (asbestos and pollution) and poor underwriting decisions on certain lines. Pricing errors, the extensive use of complex reinsurance, and unlimited commitments taken by the Names (individual investors liable on their personal assets), who had become increasingly numerous (thus creating financial overcapacity), further aggravated the situation.

In response to this very severe crisis, Lloyd’s launched, in the mid-1990s, the plan known as Reconstruction and Renewal (R&R), a set of financial and legal measures aimed at isolating and handling the old (pre-1993) losses. This led to the creation of Equitas, a vehicle designed to take over and manage these long-tail liabilities. The objective was to bring “finality” to historical commitments and allow the “new” market to restart on a sound footing. Implementation was long and legally complex, and legal “finality” was consolidated during the transfer of Equitas’ assets and liabilities to an entity backed by Berkshire Hathaway (National Indemnity Company) between 2006 and 2009.

To improve the market’s financial capacity and reduce the systemic risk linked to unlimited-liability Names, Lloyd’s authorised the entry of corporate members (limited-liability companies) from the 1994 underwriting year onwards. This change attracted institutional capital and professionalised the supply of capacity. In parallel, Lloyd’s introduced stricter requirements for funds and governance for entities underwriting through the syndicates.

Today, capacity within Lloyd’s is provided through syndicates (underwriting structures) managed by managing agents and by capital vehicles that provide financial backing to these syndicates. Since 1994, the number of dedicated and corporate vehicles has increased significantly. These structures make capital allocation more flexible and reduce direct exposure for individual investors.

The Names who had suffered historical losses progressively saw their exposures addressed (credits, settlements via R&R/Equitas and transfers). The “final step” for many of the older issues was the agreement and transfer operated with Berkshire’s subsidiary (National Indemnity), which provided additional guarantees and legally ended the remaining risks linked to historical exposures.

In simplified terms, the functioning of the market is as follows:

Accredited brokers: they bring in risks of all kinds and from all types of entities (individuals, companies, governments, reinsurance firms, etc.).

Syndicates: they underwrite (that is, they insure) the risks. Each syndicate has its own strategy and speciality or specialities: marine, aviation, cyber, catastrophe, liability, etc.

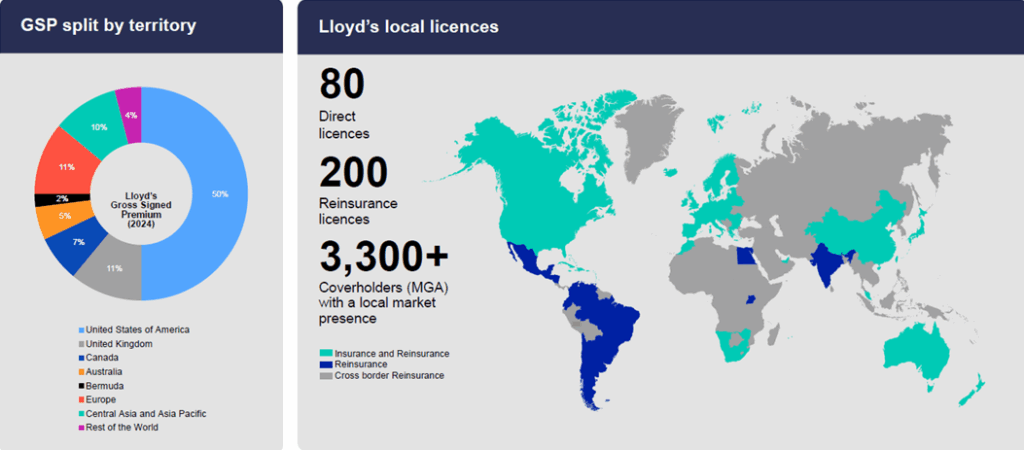

Coverholders: Lloyd’s was a pioneer of delegation as early as the late 19th and early 20th century. There are currently more than 3,300 delegated authorities. The closest French term to this concept is “agent.”

Managing agents: they manage the syndicates on a day-to-day basis (underwriting, reinsurance, claims handling, reporting, etc. — in Luxembourg one might refer to them as a fiduciaire).

Capital providers: companies (corporate members), third-party vehicles, and still a few individual Names provide the financial capacity required to cover the risks underwritten by a syndicate.

Lloyd’s Council / Corporation of Lloyd’s: this structure deals with market rules, supervision, regulatory requirements and their coordination; it manages the Central Fund (additional solvency).

Rather than a lengthy explanation, here are a few key figures.

A summary in table form is worth more than a long speech.

After the reforms of the 1990s and a long period dominated by corporate groups, we have recently seen a renewed interest from wealthy private investors (revisited Names or through structures) in uncorrelated capital, particularly between 2016 and 2023, driven by the attractive return on underwriting. However, the majority of capacity is still provided today by corporate entities and specialised funds.

The decision to establish a European entity must be understood in the context of Brexit: to continue serving European clients with a regulatory passport and to host European business underwritten locally, Lloyd’s created an insurance subsidiary in Belgium (Lloyd’s Insurance Company, also referred to as Lloyd’s Europe or LIC). This subsidiary (rated AA- by S&P), designed as a regional platform, allows direct underwriting of certain euro-denominated business and operates under the supervision of the Belgian authority (NBB – National Bank of Belgium). It ensures continuity of service for European clients after the United Kingdom’s withdrawal from the European Union.

Although Lloyd’s continues to report a substantial share of premiums coming from North America (around 50%), Europe represents approximately 11% of gross written premium as of end-2024 (growing by around 16% per year since 2020), demonstrating the strategic relevance of a European vehicle.

Traditionally, when writing about their activity, an insurance company presents the business it covers.

With Lloyd’s, this is much simpler!

Aside from life insurance, LLOYD’S INSURES EVERYTHING (OR ALMOST EVERYTHING)!

Of course, the market positions itself as the pre-eminent place for large and specialty risks: Lloyd’s remains a leader in marine, aviation, natural catastrophes, climate risks, energy, cyber and AI, war and political risks — all areas where market expertise and placement capacity are highly valued.

Even though the rise of institutional capital in operations has tightened the technical performance requirements and imposed stricter conditions on underwriters’ creativity, Lloyd’s remains a place where, when a broker presents a risk, the response “no sorry, we don’t do that” is not necessarily automatic whereas more traditional insurance companies often find it more difficult to take on such risks.

Thanks to the richness of its ecosystem (investors, brokers, underwriters, coverholders, market associations, risk-manager associations…), the market is capable of adapting to any new demand and stands at the forefront of innovation in risk management and risk transfer, both in terms of methods (facilities, algorithmic underwriting, securitisations, parametric solutions…) and insurable subject matter (new risks). The market remains forward-looking, insuring what is large in scale, complex to analyse, not yet insurable or only partially so, thereby contributing to the evolution of our economies. In other words, Lloyd’s demonstrates that insurance is an “enabler” of economic and social development.

To conclude, in summary, Lloyd’s has evolved from a 17th-century coffee house into a modern global market. The crisis of the 1980s–1990s was a turning point: it revealed the fragility of a model based solely on unlimited-liability Names and triggered profound transformations (R&R, Equitas, entry of corporate members from 1994 onwards).

Since then, the market has become more professional, significantly recapitalised, and has regained notable profitability (annual premium exceeds GBP 50 billion and annual profits have been measured in billions since the 2020s).

The establishment of an insurance subsidiary in Belgium (Lloyd’s Europe) illustrates regulatory and commercial adaptation to shifting borders (Brexit), ensuring continued access to European clients.

How can this be put?

Insurance is like air it knows no borders (despite any local regulations). The scale of the challenges we face as a human society requires both the sharing of risks and the sharing of knowledge. This has been the backbone of Lloyd’s for nearly 350 years. In this context, more than a competitor, Lloyd’s is an additive force for the countries in which it operates.

Sources :

Lloyd’s : https://www.lloyds.com/

Lloyd’s Annual Report & Aggregate Accounts 2024 (chiffres de solvabilité et performance 2024/2025) et documents internes

Rapport et archives sur la Reconstruction & Renewal (R&R) et Equitas

Dossier et note S&P sur Lloyd’s Insurance Company S.A. (Bruxelles) — création et notation (juin 2018).

Articles d’actualité et analyses sur le retour relatif des « Names » et la composition du capital (Financial Times, etc.)

https://www.investopedia.com/search?q=Lloyds

And how could one write about Lloyd’s without mentioning its anecdotes or legends, woven from equal parts boldness and imagination?

Unusual

Lloyd’s has also received insurance requests for:

abduction by extraterrestrials (policies actually issued in the 1970s!),

ghost sightings in hotels,

loss of a chance to win the lottery,

the discovery of the Loch Ness monster,

or even the Virgin Mary appearing on a piece of toast (true story)!

These contracts, often symbolic or intended for publicity, remind us that Lloyd’s is not just a financial market: it is also a laboratory for the imagination of risk.

The major losses

2005

Hurricane Katrina

Nearly USD 3 billion in losses for Lloyd’s, out of a global total of 40 billion. This event illustrated its ability to absorb major shocks while continuing to operate.

1988

Piper Alpha

Explosion of an oil platform in the North Sea. 167 deaths, USD 1.7 billion in losses — a major shock for Lloyd’s and one of the events that partly triggered the reforms of the 1990s.

1912

The Titanic

The British ocean liner was insured mainly at Lloyd’s for approximately GBP 1,000,000. The full claim was settled within a few days, strengthening the market’s global reputation for reliability.

1906

The San Francisco fire

Lloyd’s voluntarily paid claims related to the earthquake, even though the policies covered only fire. This gesture was decisive for its long-term establishment in the United States.

Hollywood (and literature)

Moonraker

Ian Fleming mentionne le Lloyd’s dans Moonraker, et Arthur Conan Doyle y fait allusion dans Le Chien des Baskerville.

Jurassic Park: The Lost World (1997)

Un personnage plaisante sur le fait que le Lloyd’s aurait refusé d’assurer les expéditions sur l’île des dinosaures !

The Crown (la série)

Plusieurs dialogues évoquent le Lloyd’s comme l’assureur traditionnel de la marine royale et des biens du palais.

The Thomas Crown Affair (1999),

le Lloyd’s est évoqué pour des œuvres d’art assurées.

The Great Gatsby (1974)

le nom du Lloyd’s est cité comme symbole d’assurance de prestige.

Lloyd’s of London (1936)

Film d’aventures historiques produit par la 20th Century Fox, avec Tyrone Power dans l’un de ses premiers grands rôles. Le film raconte (de manière romancée) les origines du marché et son rôle dans la protection des navires britanniques pendant les guerres napoléoniennes.

C’est la seule œuvre majeure qui place directement le Lloyd’s au centre du scénario.

The information presented in this article is for informational purposes only. It should not be considered as legal, regulatory or financial advice, nor as an exhaustive description of the products or services mentioned.

Looking to better understand this dynamic and diverse sector?

Discover our dossier: ‘A dynamic and diverse sector: Non-Life Insurance & Reinsurance in Luxembourg’. It features expert analyses, key figures, concrete examples, as well as testimonials and podcasts to explore the professions, products, and the role of Luxembourg as a European hub.